Fill in a Valid Cg 20 10 07 04 Liability Endorsement Template

Fill in a Valid Cg 20 10 07 04 Liability Endorsement Template

The CG 20 10 07 04 Liability Endorsement form serves as a crucial addition to the Commercial General Liability policy, specifically designed to extend coverage to additional insured parties such as owners, lessees, or contractors. This endorsement outlines essential details, including the names of additional insured individuals or organizations and the locations where covered operations take place. By modifying Section II of the policy, it ensures that these additional insureds are protected against liabilities arising from bodily injury, property damage, or personal and advertising injury linked to the actions of the primary insured or their representatives during ongoing operations. However, it is important to note that the coverage is limited by the terms of any existing contracts and does not extend beyond what is legally permissible. Additionally, specific exclusions apply, particularly concerning injuries or damages occurring after the completion of work or when the work has been put to its intended use. The endorsement also clarifies the limits of insurance, stating that any payout to additional insureds will not exceed the lesser of the contractually required amount or the available insurance limits. Understanding the nuances of this endorsement can provide peace of mind for all parties involved, ensuring that necessary protections are in place while navigating the complexities of liability coverage.

The CG 20 10 07 04 Liability Endorsement form is a crucial document in the realm of commercial general liability insurance. It designates additional insured parties and clarifies the extent of coverage provided. However, it is often accompanied by several other forms and documents that play significant roles in the overall insurance framework. Below is a list of such documents, each with a brief description.

Each of these documents plays a vital role in shaping the responsibilities and protections afforded to parties involved in commercial operations. Understanding their functions can help mitigate risks and ensure compliance with contractual obligations.

Employment Application in Spanish - The need for reliable transportation underscores workplace dependability.

Share Transfer Form J30 - Tracks the certificate numbers associated with each issued share.

In California, ensuring a proper transfer of pet ownership is vital, and utilizing the California PDF Forms for the Dog Bill of Sale can significantly simplify this process by providing a clear, legally binding document that benefits both the buyer and seller.

How to Make a Gift Card - Celebrate friendships with a certificate that conveys your care.

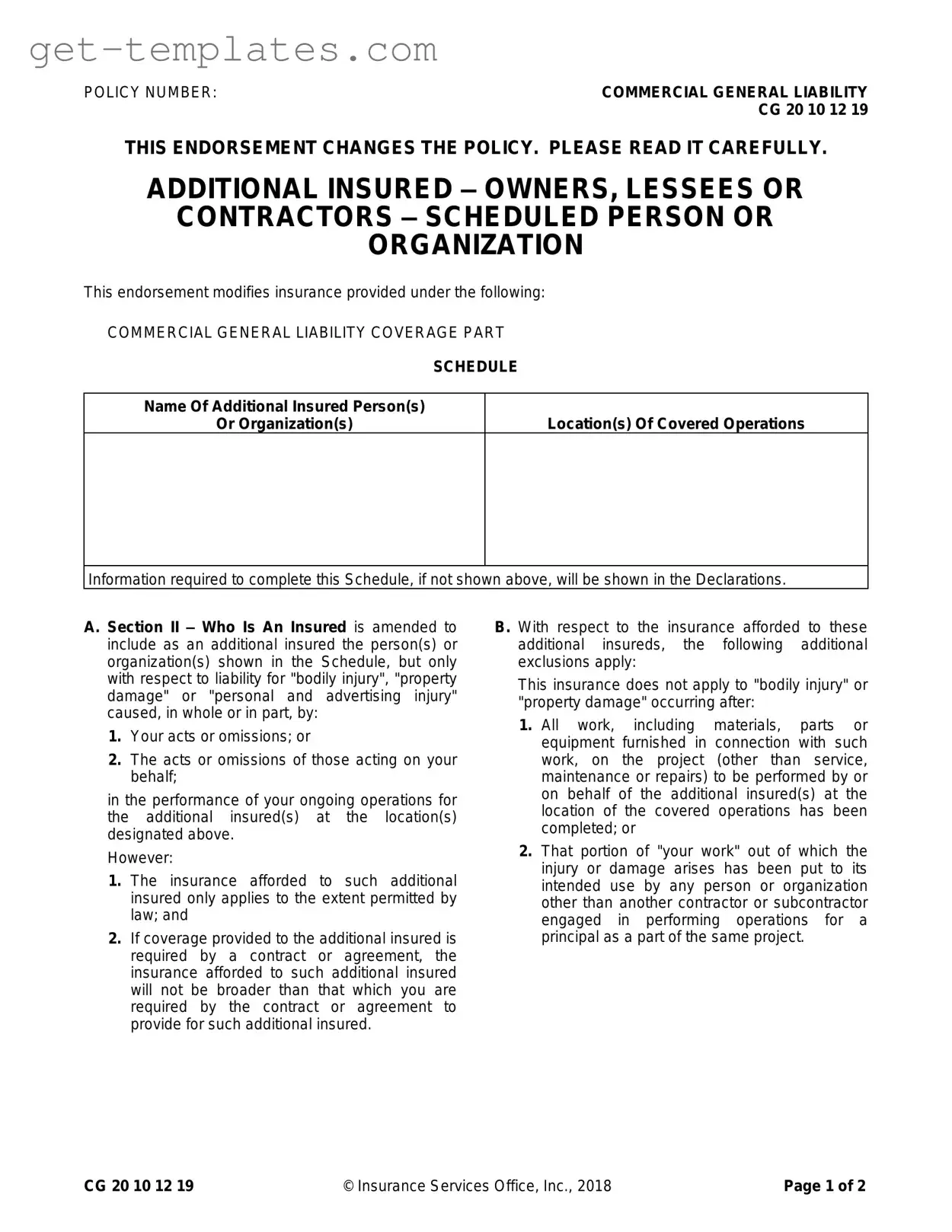

POLICY NUMBER: |

COMMERCIAL GENERAL LIABILITY |

|

CG 20 10 12 19 |

THIS ENDORSEMENT CHANGES THE POLICY. PLEASE READ IT CAREFULLY.

ADDITIONAL INSURED – OWNERS, LESSEES OR

CONTRACTORS – SCHEDULED PERSON OR

ORGANIZATION

This endorsement modifies insurance provided under the following:

COMMERCIAL GENERAL LIABILITY COVERAGE PART

SCHEDULE

Name Of Additional Insured Person(s)

Or Organization(s)

Location(s) Of Covered Operations

Information required to complete this Schedule, if not shown above, will be shown in the Declarations.

A. Section II – Who Is An Insured is amended to include as an additional insured the person(s) or organization(s) shown in the Schedule, but only with respect to liability for "bodily injury", "property damage" or "personal and advertising injury" caused, in whole or in part, by:

1.Your acts or omissions; or

2.The acts or omissions of those acting on your behalf;

in the performance of your ongoing operations for the additional insured(s) at the location(s) designated above.

However:

1.The insurance afforded to such additional insured only applies to the extent permitted by law; and

2.If coverage provided to the additional insured is required by a contract or agreement, the insurance afforded to such additional insured will not be broader than that which you are required by the contract or agreement to provide for such additional insured.

B. With respect to the insurance afforded to these additional insureds, the following additional exclusions apply:

This insurance does not apply to "bodily injury" or "property damage" occurring after:

1.All work, including materials, parts or equipment furnished in connection with such work, on the project (other than service, maintenance or repairs) to be performed by or on behalf of the additional insured(s) at the location of the covered operations has been completed; or

2.That portion of "your work" out of which the injury or damage arises has been put to its intended use by any person or organization other than another contractor or subcontractor engaged in performing operations for a principal as a part of the same project.

CG 20 10 12 19 |

© Insurance Services Office, Inc., 2018 |

Page 1 of 2 |

C. With respect to the insurance afforded to these additional insureds, the following is added to

Section III – Limits Of Insurance:

If coverage provided to the additional insured is required by a contract or agreement, the most we will pay on behalf of the additional insured is the amount of insurance:

1.Required by the contract or agreement; or

2.Available under the applicable limits of insurance;

whichever is less.

This endorsement shall not increase the applicable limits of insurance.

Page 2 of 2 |

© Insurance Services Office, Inc., 2018 |

CG 20 10 12 19 |

The CG 20 10 07 04 Liability Endorsement form is used to add additional insured parties to a commercial general liability insurance policy. This endorsement ensures that specific individuals or organizations are covered under the policy for certain liabilities that may arise during the performance of ongoing operations. It provides clarity on who is protected and under what circumstances.

Individuals or organizations listed in the endorsement schedule qualify as additional insureds. They are protected against liability for bodily injury, property damage, or personal and advertising injury that results from the acts or omissions of the primary insured or those acting on their behalf during the specified operations.

The coverage for additional insureds is limited in several ways:

The endorsement specifies that coverage does not apply to bodily injury or property damage occurring after all work related to the project has been completed. This includes all materials, parts, or equipment involved in the project, except for service, maintenance, or repairs.

Yes, there are specific exclusions. For instance, if the injury or damage arises after the work has been put to its intended use by someone other than another contractor or subcontractor, the additional insured will not be covered. This means that the timing and context of the work are critical in determining coverage.

The limits of insurance for additional insureds are determined by the lesser of two amounts: the amount required by the contract or the available limits under the primary insured's policy. Importantly, this endorsement does not increase the overall limits of insurance provided by the policy.

Yes, it is essential to read the endorsement carefully. The wording can significantly affect coverage, and understanding the terms will help ensure that all parties know their rights and responsibilities. Clarity in insurance coverage can prevent disputes and provide peace of mind.

Here are some key takeaways regarding the use of the CG 20 10 07 04 Liability Endorsement form:

| Fact Name | Details |

|---|---|

| Policy Number | CG 20 10 12 19 |

| Purpose | This endorsement adds additional insured coverage for owners, lessees, or contractors. |

| Coverage Type | It modifies the Commercial General Liability Coverage Part. |

| Additional Insured | Includes individuals or organizations specified in the schedule for liability related to bodily injury or property damage. |

| Coverage Conditions | Coverage applies only to acts or omissions during ongoing operations for the additional insured. |

| Exclusions | Excludes coverage for injuries or damages after project completion or intended use. |

| Limits of Insurance | Payment is limited to the lesser of contract-required amounts or available insurance limits. |

| Governing Law | Varies by state; check local regulations for specific requirements. |

| Endorsement Effect | This endorsement does not increase the limits of insurance provided. |